- Mortgage rates are on the rise in 2022.

- If you still want to pull some cash out of your home, here are your options.

For many homeowners, the pandemic offered an unprecedented opportunity to build wealth. Those opportunities still exist, even though they are getting harder to come by.

Thanks to skyrocketing housing prices, the amount of home equity is at an all-time high.

As of the third quarter of last year, homeowners held $9.4 trillion in equity to tap, the largest amount ever recorded, according to the most recent data from Black Knight, a mortgage technology and research firm.

For the average homeowner, that’s nearly $178,000 in equity available to tap before hitting a maximum combined loan-to-value ratio of 80%, according to Black Knight Data & Analytics President Ben Graboske. Most lenders require that you keep at least 20% equity in your home, if not more, as a cushion in case home prices fall.

Taking advantage of all that extra cash, however, becomes more difficult as interest rates rise.

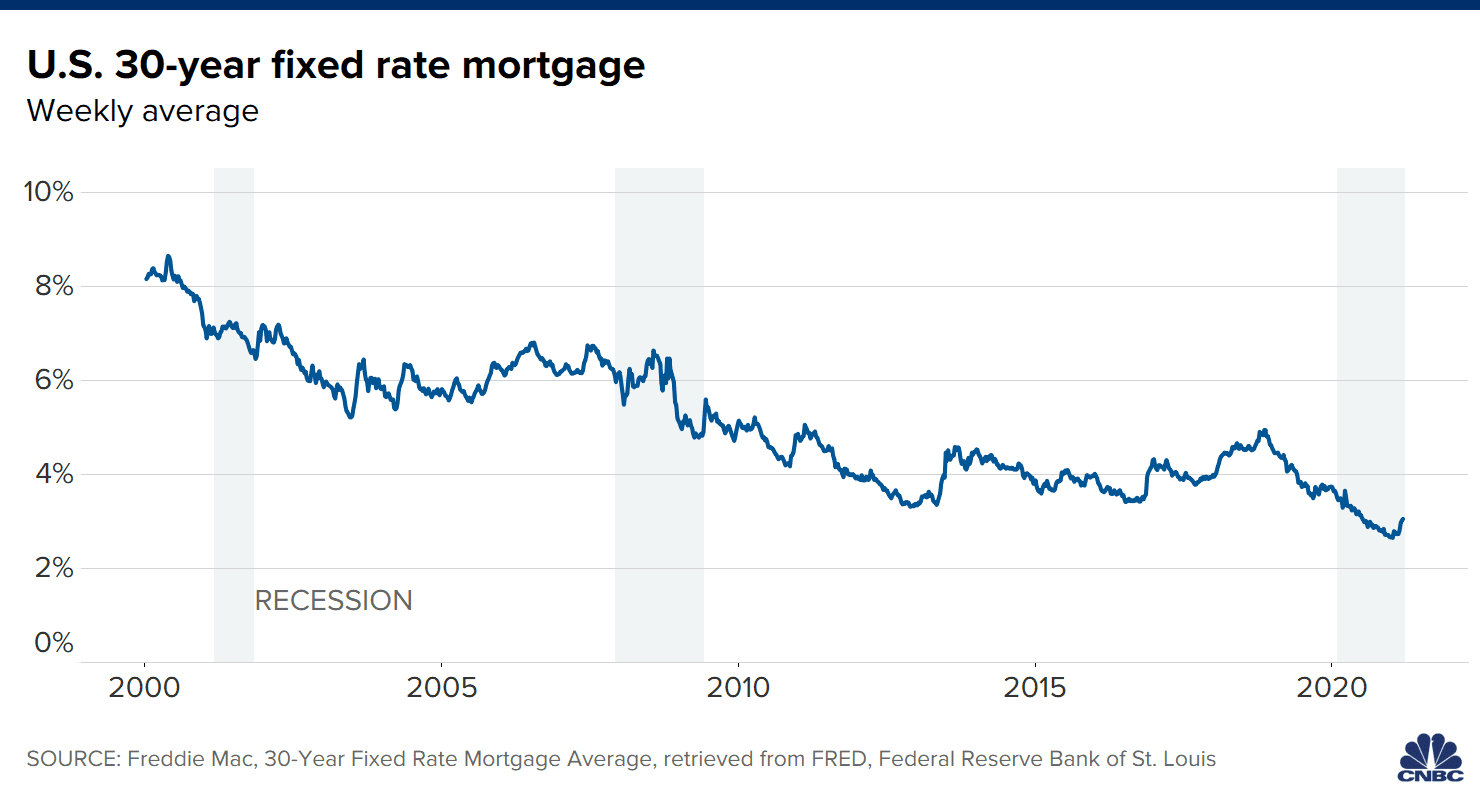

Mortgage rates are already heading higher, thanks, in part, to inflation and the Federal Reserve.

Recent inflation reports reached their highest levels in decades. The Consumer Price Index, which measures the cost of a wide-ranging basket of goods and services, surged 6.8% year over year, the fastest rate since June 1982.

In response, the Fed signaled it will dial back its economic help more quickly than anticipated, with Fed officials seeing as many as three rate hikes this year, two more next year and another two in 2024.

That is causing long-term fixed mortgage rates to rise. Already, the average rate on a 30-year fixed mortgage is up to 3.33% — now about half a percentage point higher than a year ago.

“With higher inflation, promising economic growth and a tight labor market, we expect rates will continue to rise,” said Sam Khater, Freddie Mac’s chief economist.

By the end of 2022, average mortgage interest rates will be as high as 4%, according to Jacob Channel, senior economic analyst at LendingTree.

“There is still time for people to tap into their home equity with either a home equity loan or a refinance,” he said. However, “the window of opportunity is closing.”

The best ways to tap your home for cash

When rates are low, a so-called cash-out refinance is particularly attractive. Homeowners can refinance their current mortgage, take out a bigger mortgage and lower the interest payment at the same time.

Even now, applicants with good credit may get a rate at or below 3%.

“If you can get it in the next few months, hopefully before summer, you might still be able to find a really good deal,” Channel said.

Homeowners may also be able to deduct the interest on the first $750,000 of the new mortgage if the cash-out funds are used to make capital improvements. However, since fewer people now itemize deductions on their tax returns, most households won’t benefit from this write-off.

“You might still be able to find a really good deal.”

Jacob Channel SENIOR ECONOMIC ANALYST AT LENDINGTREE

Alternatively, a home equity line of credit, or HELOC, which is a revolving line of credit but with better rates than a credit card, is another way to borrow against the equity you’ve accumulated in your home.

The average interest rate on this type of credit is around 5%. Credit cards charge roughly 16%, on average.

Fewer banks offered this option during the height of the Covid pandemic, when lenders tightened their standards to reduce their risk. Access to HELOCs has improved, although the most preferable terms still go to borrowers with higher credit scores and lower debt-to-income ratios.

Deciding between a cash-out refinance or HELOC will depend on how much equity you have in your home and your time frame, according to Christian Wallace, head of real estate services at mortgage firm Better.

For example, if you want a shorter-term commitment and don’t have that much equity to tap, a HELOC may be a better bet. Alternatively, if you can refinance and reduce your interest rate by at least half a percentage point, then a cash-out could work in your favor.

“Every situation is going to be different,” Wallace said.

Keep in mind that different lenders will also offer different terms and interest rates, she added. Wallace recommends talking to at least three mortgage companies or loan officers, as well as weighing all the costs before deciding what makes the most sense.

Jessica Dickler

@JDICKLER